Subscribe

SubscribePresented below is our summary of significant Internal Revenue Service (IRS) guidance and relevant tax matters for the week of October 17, 2022 – October 21, 2022.

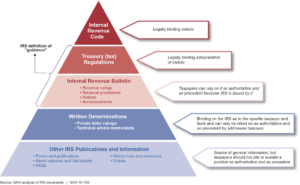

October 17, 2022: The IRS released Internal Revenue Bulletin 2022-42, which highlights the following:

- Notice 2022-45: This notice extends the deadline for amending an eligible retirement plan to reflect the Coronavirus Aid, Relief, and Economic Security Act (CARES Act) and the Taxpayer Certainty and Disaster Tax Relief Act of 2020 (Relief Act). Both allow for special tax treatment with respect to a coronavirus-related distribution or a qualified disaster distribution.

- Notice 2022-43: This notice provides guidance regarding the extension of the four-year replacement period for livestock sold because of the drought. The relief extends to 44 states, two US territories and two independent nations. It generally applies to capital gains realized on sales of livestock held for draft, dairy or breeding purposes.

October 17, 2022: The IRS announced its continued support to fight fraud targeting charities, businesses and individuals during Charity Fraud Awareness Week, which was October 17 to October 21. The IRS estimates that charities lose 5% of their revenue each year to fraud.

October 17, 2022: The IRS released Tax Tip 2022-158, reminding taxpayers to review their withholdings and estimated tax payments.

October 17, 2022: The IRS released Revenue Ruling 2022-20, providing various prescribed rates for federal income tax purposes for November 2022.

October 17, 2022: The IRS released Notice 2022-54, which provides guidance on the corporate bond monthly yield curve and corresponding spot segment rates and the 24-month average segment rates for October 2022. The notice also provides guidance as to interest rates on 30-year Treasury securities and 30-year Treasury weighted average rates.

October 17, 2022: The IRS reminded families that they may be eligible for the Child Tax Credit if they claim at least one child as their dependent. The IRS specifically urges grandparents, foster parents or people caring for siblings or other relatives to check whether they are eligible to receive the 2021 Child Tax Credit.

October 18, 2022: The IRS released Tax Tip 2022-159, suggesting that taxpayers with an outstanding tax bill consider making an Offer in Compromise. An Offer in Compromise is an option for taxpayers who cannot pay their full tax liabilities or in situations where paying the balance would create financial hardship.

October 18, 2022: The IRS announced the 2023 annual inflation adjustments for more than 60 tax provisions, including the tax rate schedules and other tax changes. The Inflation Reduction Act of 2022 is extending certain tax breaks related to energy for the first time in 2023. The standard deduction for a married couple filing jointly and single and married taxpayers filing separately is also increasing. All of the 2023 adjustments can be found in

Continue Reading

read more

")

")